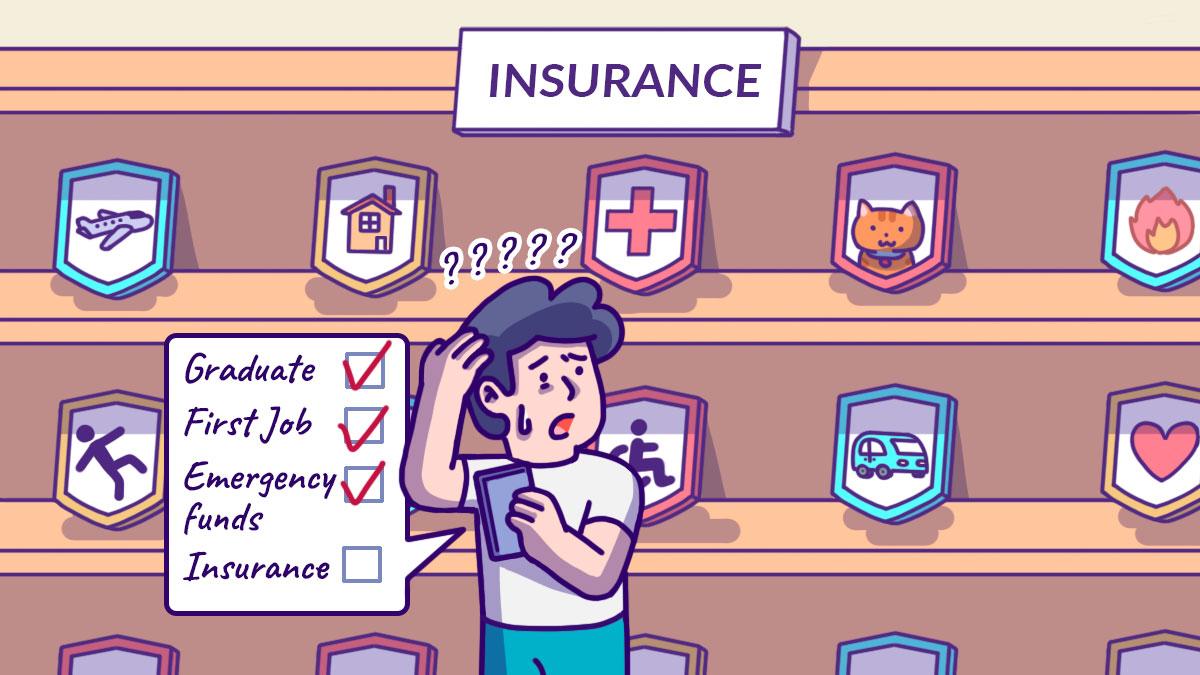

The importance of being insured

While you’re probably more excited to start building your savings — because the prospect of getting a lump sum of money in a decade or two is thrilling — any financial planner worth their salt will recommend some basic protection plans first. Why? Because it gives you the financial backup you need in case of emergencies, especially those of the medical kind. You may be thinking: Aren’t I just throwing money down the drain though, since I won’t get any returns on the premiums for protection plans unless some disaster were to befall me. And who wants that? However, that is precisely why you need protection plans. It’s for the off chance that something bad were to happen and you would require large sums of money. Surely you wouldn’t want one incident to wipe out your savings, or even worse, lend you in debt. With the right insurance, you don’t need to worry about your cashflow should you lose the ability to continue working due to critical illness or severe injuries. So what kind of protection do first jobbers need? Here are some protection plans that you should ensure you have.1. Hospitalisation

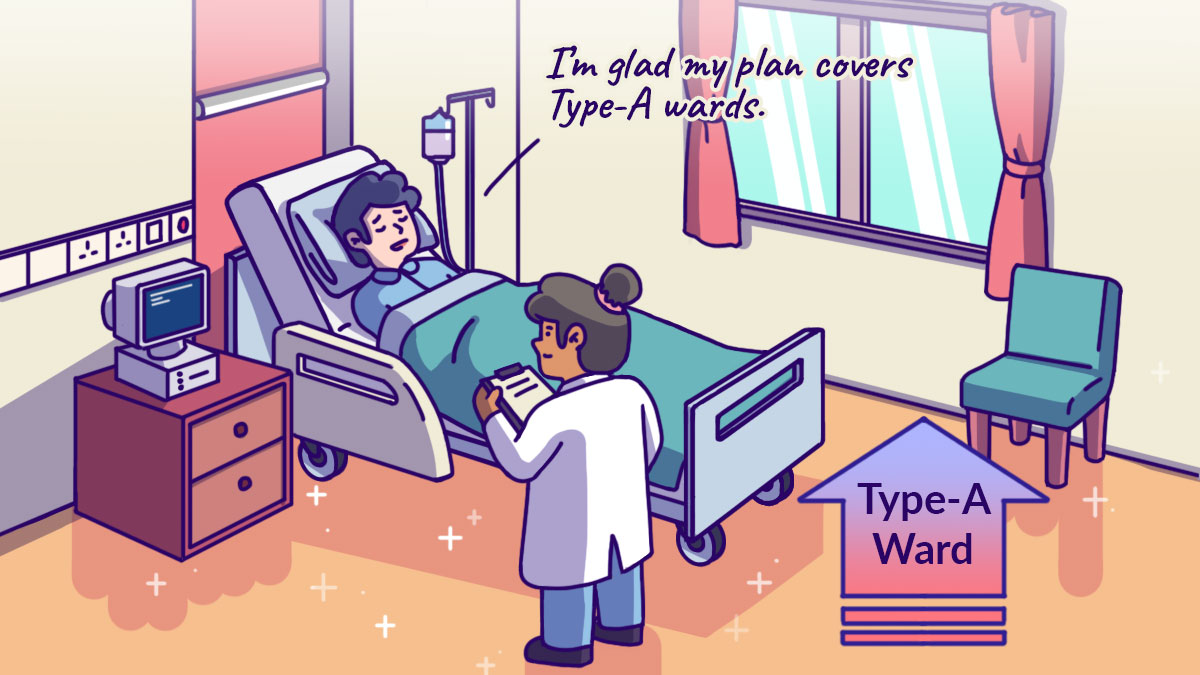

Yes, all Singaporeans and PRs are covered under a compulsory government health insurance plan called MediShield Life. And this helps to pay for large hospital bills and selected costly outpatient treatments, such as dialysis and chemotherapy for cancer. So, you might be wondering why you should still get a private hospital plan. Well, the government plan is pegged at B2/C-type wards. If you choose to stay in a higher tier ward or a private hospital, you’ll still get a payout but it will only cover a small proportion of the bill. If you get a standard Integrated Shield Plan (IP) provided by private insurers, you can cover a stay in B1/A-type wards, as well as private hospitals — after deductibles and co-payments. For first-jobbers, an IP has to be one of the staples in your portfolio because it subsidises your hospitalisation bills (up to private hospitals) and eases the burden on your finances and MediSave. This is especially important since you don’t want to drain your savings or your MediSave too early in life. Being hospitalised may seem like an unlikely event for young adults, but it’s always better to be prepared because when you might find yourself staring down a bill that’s a couple hundred thousand dollars.