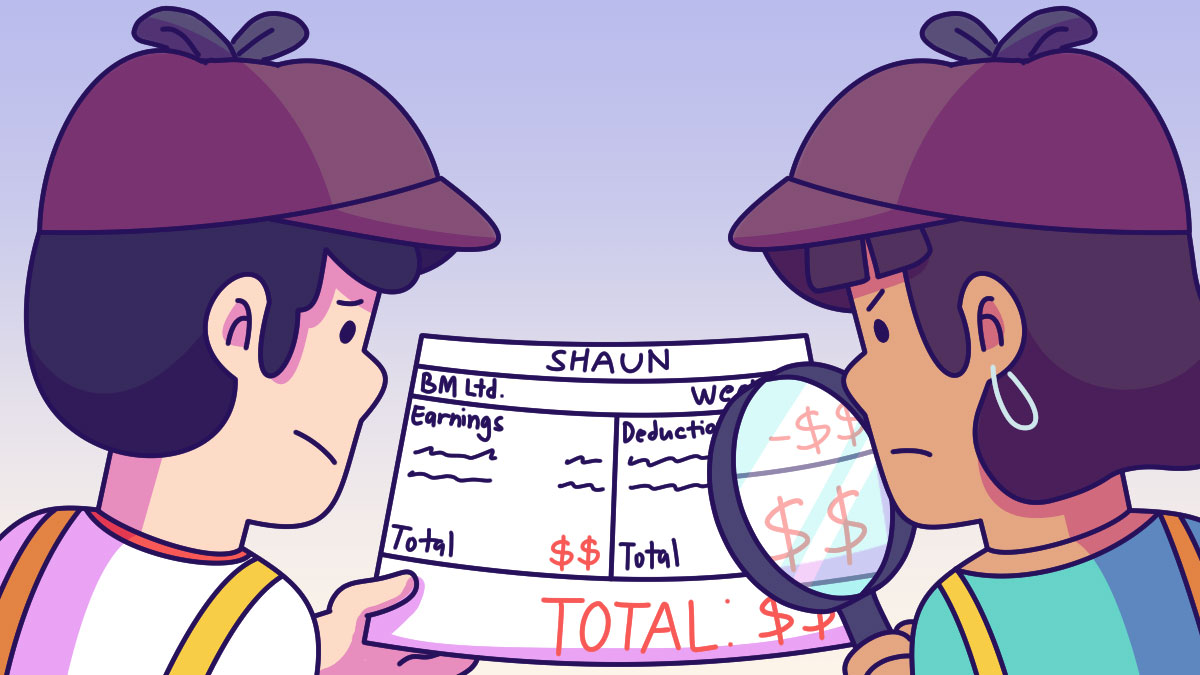

You might think, "What's the big deal with pay slips? They are often overlooked as mundane documents, but your pay slip actually contains a wealth of data crucial for making informed financial decisions. Pay slips are essentially income report cards, showing how much you earn, what benefits you receive, and where your money goes before it even hits your bank account. Not understanding your pay slip can put you at a disadvantage when negotiating compensation effectively. Your pay slip consolidates your compensation package, including your base salary, bonuses, commissions, and additional benefits or perks. Without knowing what you are entitled to currently, you may struggle to build a strong case for negotiating better compensation during performance reviews or job transitions which can lead to costly financial mistakes. Here are some financial tips to help you understand your pay slip.

#1 Understanding pay slip geekspeak

Pay slips are filled with abbreviations and codes that can seem confusing at best and incomprehensible at worst. Understanding the language used is the first step to making sense of it. Take the time to learn common terms and acronyms such as 'Gross Income' and 'Net Income'. Also, familiarise yourself with phrases related to your specific pay, such as bonuses, commissions, allowances, or benefit deductions. You can get a list of the important phrases from your HR Department.Knowing the payroll lingo will help you accurately interpret details about your earnings, taxes, and overall compensation. Here are some common terms that you will find in your pay slip:

Basic Salary | Fixed amount paid regularly for standard work hours |

Allowances | Additional payments for specific purposes (e.g. transport, food) |

Gross Salary | Total earnings including allowances before deductions |

Deductions | Amounts subtracted from gross salary (e.g. CPF contributions) |

Net Salary | Amount employee receives after all deductions from gross salary |

Overtime Pay | Additional compensation for hours worked beyond normal working hours |

Reimbursements | Repayment for work-related expenses incurred by the employee |

Income Tax | Mandatory contribution to the government based on an employee's taxable income |

#2 Verify total income

Once you understand what your pay slip says, the next step is to check your total income. This includes your basic salary plus any additional earnings, such as bonuses, commission, and overtime pay. Pay close attention to the overtime pay section and cross-check it against your hours worked and the terms of your employment contract. Ensure you're receiving proper compensation for all the extra hours worked beyond your regular schedule.Small mistakes in overtime calculations can accumulate, potentially resulting in underpayment that can take time to unravel.

#3 Add all employment benefits

Next, don't forget to count all your employment benefits. These can be fixed benefits, like health insurance or a company car, and variable benefits, such as performance bonuses.Including these in your calculations ensures you're accounting for all the perks your job offers, which can significantly boost your overall compensation package and provide a more accurate tool for comparison with other roles.

#4 Subtract deductions to arrive at net income

After totalling your income and benefits, subtract what gets taken out of your pay packet. This includes taxes, retirement contributions, and insurance premiums. These deductions can really cut into your pay, so it is worth making sure they're correct. Once you've subtracted all the proper deductions from your total earnings, you'll be left with your net income - this is the real amount you take home. Use this net pay figure as the basis for creating a budget, managing your finances and making financial decisions effectively, but don’t forget to add the benefit costs back into your budget.

#5 Calculate taxable income accurately

Your taxable income is the portion of your earnings you must pay taxes on. It's important to know what income is taxable and what isn't. Things like your base salary, bonuses, and commissions are usually taxable above $20,000. However, certain benefits like retirement contributions or employer-paid insurance premiums may not be taxed. Correctly calculating your taxable income ensures you pay the proper amount of taxes - no overpaying or underpaying. This helps avoid penalties or surprise tax bills down the road.

#6 Ensure consistency and identify discrepancies

Compare your current pay slips to previous ones and look for anything that seems off or inconsistent. Employers can accidentally make mistakes like wrong deduction amounts, miscalculated overtime pay, or missing bonuses. If you spot any inconsistencies, raise them immediately. These errors may seem small but can really add up and cost you money over time if left unchecked. Regularly cross-checking your pay slips helps catch and fix issues before they become a bigger financial headache.

This content is part of the Temasek – Financial Times Challenge, a financial literacy education series in Singapore for youths.