Article

Are You Ready for the Inflation War in Singapore?

Inflation is this nine-letter bad word that's on everyone’s lips these days. From the United States and United Kingdom to Philippines and Malaysia, prices of almost everything in our daily lives are going up.Here in Singapore, the price of chilled poultry has risen 33.6%, eggs by 22.8% and electricity by 26.4%, compared to last year according to the Singapore Department of Statistics report on 22 July 2022.Even the popular Japanese retail chain, Daiso, couldn’t escape the impact of inflation this year. The chain best known for being a S$2 store in Singapore shared that the heightened price of raw materials and logistics has forced it to pass on that added operating cost to the consumer. Daiso now charges from S$2.14 to S$25.47. That's a 1273.5% price increase from S$2 to S$25.47.We decided to dig deeper into the inflation conversation and share what it all means to you and your finances.Let's start with "What is inflation"? The International Monetary Fund or IMF describes Inflation as "the rate of increase in prices over a given period of time. Inflation is typically a broad measure, such as the overall increase in prices or the increase in the cost of living in a country". Basically, everything you buy becomes more expensive as time goes on. Or another way of looking at it, your dollar is worth less and less over time because your dollar can’t buy as much things as it used to. As an example, S$1 can buy you two cups of coffee at the hawker 20 years ago while S$1 may not even get you a cup today. Theoretically, inflation can be good for the economy when prices increase at a steady rate each year. But in 2022, we’re seeing high inflation rates that has made our cost of daily living a lot more expensive in a short span of time.How much inflation is there? Inflation from July 2022 to August 2022 was 0.944% and the inflation rate year over year is 7.465% based on information from the Singapore Department of Statistics. It was only 2.4% year over year in August 2021. If you are calculating in terms of chicken rice, your S$3.50 plate of chicken rice has inflated to at least S$4.50. That’s a 28.57% increase! Where did all this inflation come from? Inflation or overall price increase is triggered by cost-push factors and demand-pull factors. The increase in cost of Daiso's production is an example of a cost-push factor that triggers inflation. A demand-pull factor is when consumers are willing to pay more for certain goods and therefore their demand is “pulling” up prices.How does inflation hurt your savings? An increase in inflation from 1% to 3% means a 45.8% fall in your retirement savings over thirty years. Using the Central Provident Fund (CPF) Retirement Account as an example, S$270,700 in retirement savings is reduced to S$146,719 by the time you hit 65 years old. A 3% annual inflation rate will also reduce your purchasing power by almost 60% over thirty years. Therefore, your S$1 can only buy 40 cents worth of goods in 30 years. The Inflation War Fans of Walt Disney's Avengers Movies will recall Thanos' search for the 6 Infinity Stones. By placing them into the Infinity Gauntlet, he can make right the universe by halving its population, thus triggering the Infinity War. Applied to real life, these stones represent the six asset classes of Cash, Bonds, Stocks, Real Estate, Commodities and Cryptocurrencies in an Inflation Gauntlet held by each Central Bank. A central bank is a country’s government organisation that manages and controls that country’s money supply. The central bank of Singapore, for example, is the Monetary Authority of Singapore (MAS). Central Banks have started an Inflation War with their Inflation Gauntlets. Instead of half the world's population disappearing, half of the money that’s in the economy may disappear at the snap of their fingers. And there has been a lot of finger snapping this year with the US Fed raising interest rates, which both directly and indirectly triggered Singapore’s Inflation Gauntlet, thereby creating a larger black hole in our wallets. We end up with less savings to pay for the higher cost of food, housing, and transport. The Inflation War is undoubtedly here in Singapore. It is already brewing on our roads, in our supermarkets, our restaurants, our workplaces and our homes. You'll be amazed how little your S$50 can buy these days. You may start considering downsizing and find new ways to diet simply by looking at the price of food. If you're thinking of starting a family, inflation is going to make you think twice. It may transform many of us into cheapskates. And there's no escaping if you have basic needs, a job, a business, a mortgage and/or children. In a worst-case scenario, this inflation war can plunge Singapore into a prolonged period of instability. Now that you know what inflation means, should you be concerned about inflation? Here’s what you can do to combat inflation and save your wallet if your answer is a resounding yes.

How to Get Through the Festive Season with Your Finances Intact

Feeling the Pinch of Inflation? Ask Yourself These 4 Important Questions To Better Manage Your Money Amidst Rising Costs

Why Doing Everything Yourself May Not Be The Best Idea

5 Smart Ways To Reduce Your Monthly Petrol Bill

What You Really Need to Know about Singapore T-bill

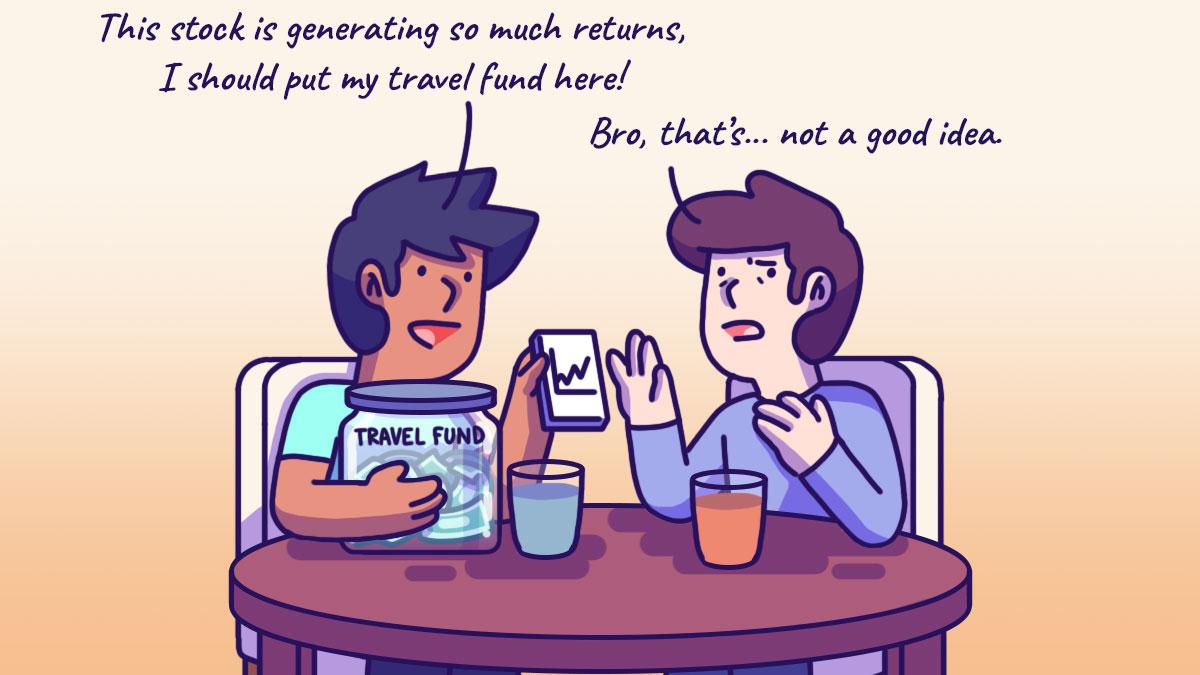

Why You Shouldn’t Put Your Travel Fund in The Stock Market: How to Plan and Invest for Your Short-Term Goals

How To Manage Medical Costs in Singapore Amidst Inflation

Does Reviewing Your Insurance Coverage Really Matter?

Financial Services on Web3: Decentralised Finance (DeFi)